.svg)

South Korea’s Financial Services Commission (FSC) and the Korea Financial Intelligence Unit (KoFIU) are advancing a targeted set of reforms to the country’s anti-money laundering framework following a review of the Act on Reporting and Using Specified Financial Transaction Information. Rather than overhauling the system, authorities aim to close operational gaps identified through supervision, particularly as digital asset markets expand and process growing volumes of bank-linked transactions. The reforms focus on improving transaction transparency, strengthening investigative tools and clarifying reporting obligations as South Korea prepares for its next Financial Action Task Force mutual evaluation in 2028.

The bigger picture

South Korea’s proposed amendments reflect a financial system that has expanded beyond the environment in which the original AML framework was designed in 2001. The expansion of digital finance, online payment platforms and virtual asset markets has transformed the volume and velocity of financial flows across the economy. Transaction reporting volumes have increased significantly as regulators rely more heavily on data-driven monitoring to identify suspicious activity.This shift is visible most clearly in the rapid growth of suspicious transaction reporting and the increasing share of activity linked to digital financial services and virtual asset platforms.

- Increased financial activity begets larger suspicious transaction volumes

Suspicious transaction reporting illustrates the scale of change. Authorities received approximately 1.3 million reports in 2025 compared to just 1,744 in 2003. The increase reflects both the expansion of financial activity and the growing reliance on large datasets to identify potential money laundering risks.

These developments have exposed limitations within the existing regulatory framework, which was originally designed around conventional banking activity. Policymakers are therefore introducing targeted reforms that expand investigative capabilities, strengthen digital asset oversight and improve transparency across financial transactions.

- Digital assets forcing the regulatory hand

Digital asset markets sit at the centre of the reform agenda. South Korea hosts one of the world’s most active cryptocurrency trading environments, with exchanges processing significant transaction volumes that interact closely with domestic banking infrastructure.

Regulators are prioritising greater visibility into these flows. Travel Rule obligations are expected to expand and additional scrutiny will apply to transactions involving overseas exchanges and private wallets. Authorities are also developing a dedicated AML framework for stablecoin issuers, recognising their growing role in digital payments and settlement activity.

- Strengthening investigative and enforcement tools

The FSC and FIU are also looking to strengthen enforcement capabilities during financial crime investigations. Supervisory authorities have identified procedural limitations that can delay intervention when suspicious financial activity is detected.

How does this change things?

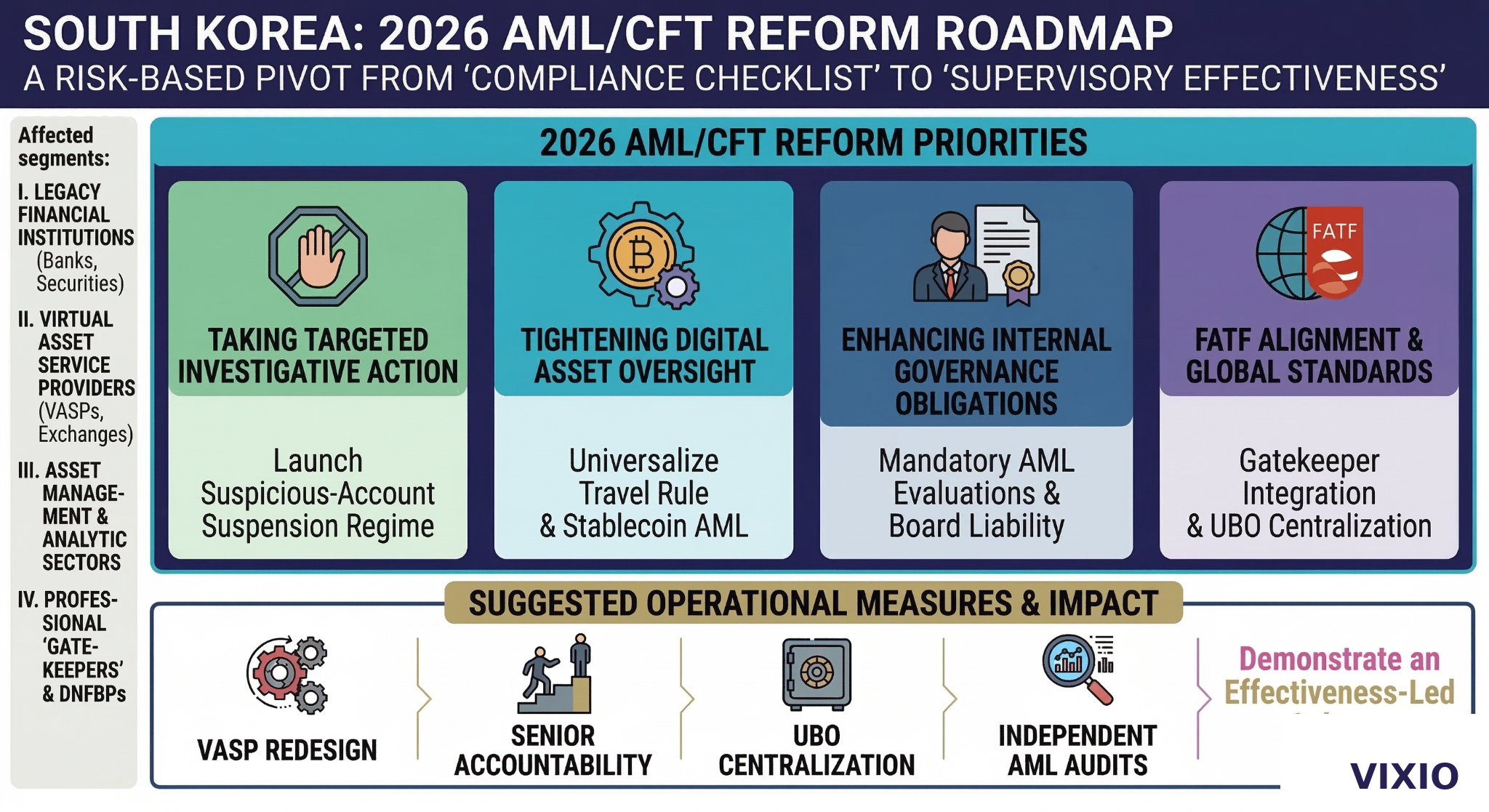

The amendments introduce several targeted measures that expand supervisory authority while increasing compliance expectations across financial institutions, digital asset firms and certain professional service providers.

- Suspicious account suspension

Authorities will be able to suspend accounts suspected of containing criminal proceeds when investigative agencies identify links to serious offences including:

- Narcotics trafficking.

- Illegal gambling operations.

- Organised financial crime.

- Terrorism financing.

The objective is to prevent illicit funds from being moved during active investigations.

- Widened scope of financial transaction restrictions

Existing restrictions largely focus on entities associated with terrorism or weapons proliferation. The revised framework extends these powers to international criminal organisations, enabling authorities to block financial activity linked to transnational crime networks.

- Expanded Travel Rule requirements

Digital asset oversight will tighten under the proposed amendments. Current regulations require virtual asset service providers to transmit sender and recipient information only for transfers exceeding KRW 1 million. Regulators plan to extend these obligations to lower-value transactions while strengthening verification requirements.

Expected changes include:

- Applying Travel Rule data transmission to smaller transactions.

- Requiring receiving exchanges to verify sender and recipient information.

- Introducing stricter data retention requirements for transaction records.

- AML framework for stablecoins and private wallets

Authorities are also developing a dedicated AML framework for stablecoin issuers. Proposed obligations include:

- Customer due diligence requirements.

- Suspicious transaction reporting obligations.

- Internal AML governance and risk management systems.

Transactions involving private wallets and overseas exchanges will also face enhanced due diligence requirements.

- Mandatory AML system implementation evaluations

Supervisory oversight of financial institutions will become more formalised. The AML System Implementation Evaluation currently operates on a voluntary basis, but regulators intend to make participation mandatory while introducing sanctioning powers for institutions that fail to submit required information or provide inaccurate reporting.

- Centralised beneficial ownership verification

The reforms will also establish a centralised system for verifying corporate beneficial ownership information. Financial institutions, regulators and law enforcement agencies will be able to cross-check ownership structures more efficiently, reducing the misuse of shell companies and nominee arrangements.

- Expansion of AML obligations to professional intermediaries

AML obligations may also extend beyond the financial sector. Lawyers, accountants and tax advisers could become subject to customer due diligence and suspicious transaction reporting requirements when providing certain financial or corporate services.

What does this mean for financial institutions?

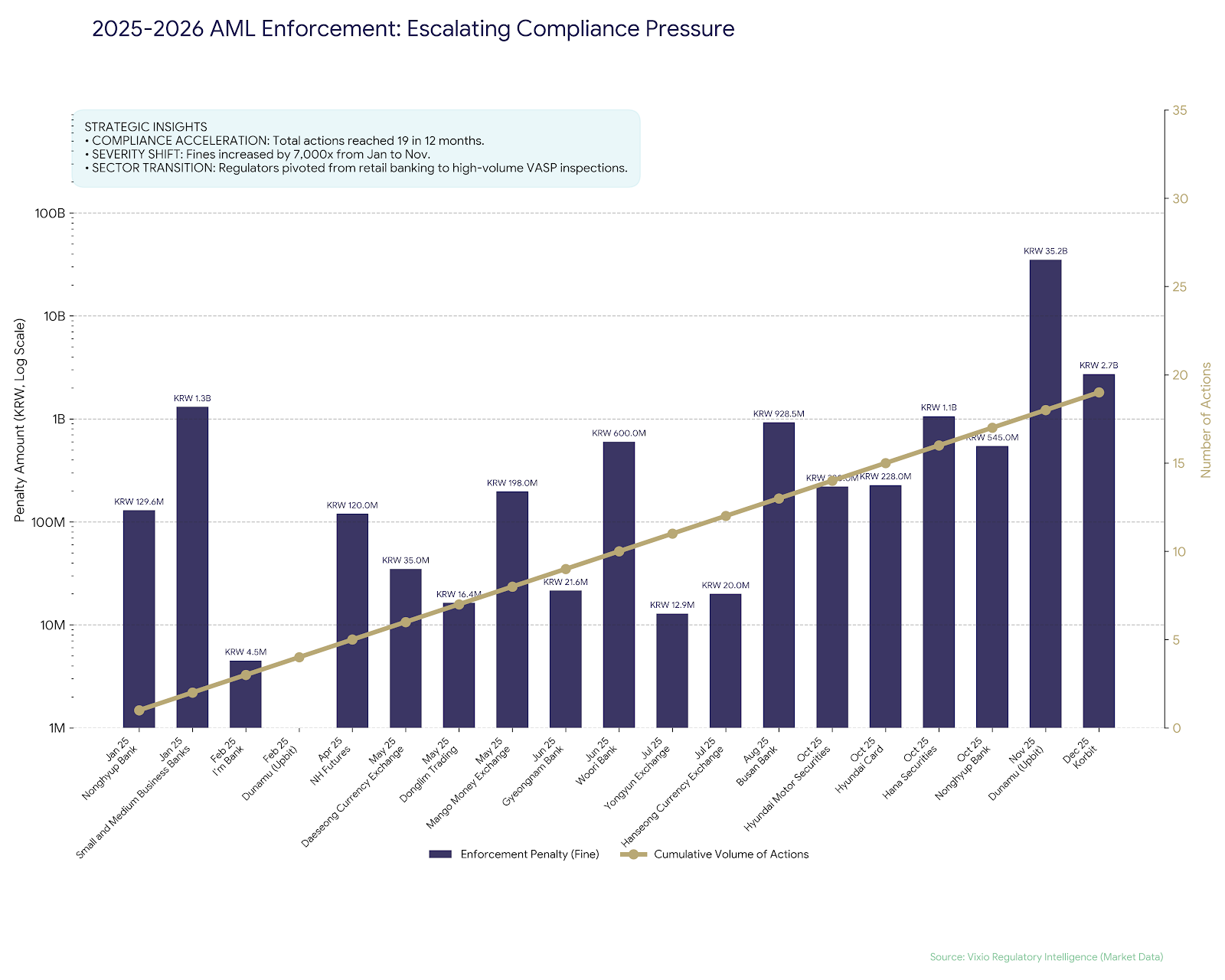

Under the reforms, financial institutions, payment providers and digital asset firms in South Korea should expect closer supervision and rising enforcement. Recent enforcement activity shows penalties becoming larger and more concentrated among virtual asset exchanges and electronic financial service providers. Many cases involve structural weaknesses in AML governance and monitoring systems rather than isolated breaches. The pattern suggests regulators are increasingly willing to impose significant financial penalties where high-volume digital transaction flows are not adequately controlled. The diagram below shows the rise in AML related enforcement activity in South Korea.

Looking ahead

The reforms under development represent a structural strengthening of South Korea’s financial crime framework as digital asset activity expands and cross-border financial crime becomes more sophisticated. Regulators are likely to combine stronger supervisory powers with increasingly data-driven monitoring capabilities in the years ahead.

Transaction monitoring resilience, clear governance accountability and effective beneficial ownership transparency will therefore become central components of financial institutions’ operational risk management as South Korea prepares for its FATF mutual evaluation in 2028.