.svg)

Participants identified several foundational questions for the UK cryptoasset framework, including areas of regulatory treatment and infrastructure design that must be addressed for stablecoins to operate at scale as payment instruments.

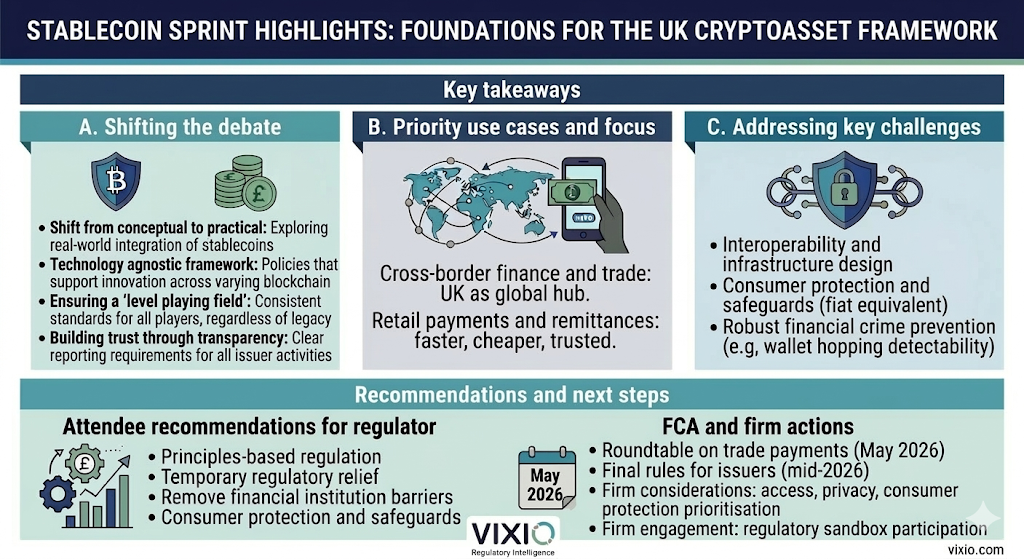

The Financial Conduct Authority’s (FCA) Stablecoin Sprint, held over two days in early March 2026, brought together regulators, traditional financial institutions and crypto innovators to discuss how the UK can safely scale stablecoin adoption for payments and remittances.

The event was intended to generate actionable insights to inform the regulator’s thinking and help shape the future of stablecoin payments in the UK.

The focus was on developing a regulatory framework that unlocks faster, cheaper and trusted payments, while ensuring that consumers and markets remain protected.

The sprint centred on retail payments and remittances, and tested different ideas and business models against challenges such as making payments faster, cheaper, interoperable and trusted, and ensuring consumer protection.

On a strategic level, the FCA’s goal is to take the opportunity presented by digital assets to reinforce the UK’s position as a leading global hub for international money movement and trade.

Attendees broke into working groups and together mapped out end-to-end user journeys, stress-tested potential risks such as financial crime and translated their findings into practical priorities for future policy.

Alongside the working sessions, the sprint also featured FCA keynotes and remarks from the economic secretary to the Treasury, Lucy Rigby.

Catarina Veloso, director, regulatory and compliance at Notabene, told Vixio that, “Overall, the sprint highlighted that while the policy conversation around stablecoins is maturing, several foundational questions – from regulatory treatment to infrastructure design – still need to be addressed before stablecoins can operate at scale as payment instruments.”

Becoming credible payment instruments

The FCA intended the Stablecoin Sprint to act as a bridge between its earlier proposals and its upcoming final rules for the crypto sector, and the event seems to have been useful in moving the conversation along.

Tom Rhodes, chief legal officer at Agant, told Vixio, “The reason the sprint was such a success was because it focused on the practical realities of how stablecoins operate. The policymakers in attendance were open to understanding what the industry needs. The FCA deserves a lot of credit.”

By bringing the industry together to map out business models and risk mitigations, the regulator was seeking to ensure that the forthcoming mid-2026 rules are rooted in practical implementation and can scale innovation safely.

According to Veloso, “What stood out from the discussions was that the debate is increasingly moving beyond whether stablecoins should exist, and toward what needs to evolve for them to function as credible payment instruments.”

One area of consensus was that stablecoins will not become a viable payment instrument if the law classifies and treats them as cryptoassets – to work for everyday payments, they need “money-like” treatment.

This includes cash-equivalent accounting, clear payment permissions and tax clarity. For example, this would mean that consumers using stablecoins to pay for goods would not be subject to capital gains tax.

Participants widely agreed that cross-border finance and trade are the core use cases for stablecoins, and that the UK must reflect and connect to the global ecosystem.

Another key theme was trust, with participants noting that policymakers must ensure that consumers using stablecoins have access to the same safeguards and protections they expect from traditional fiat payments.

This links to a need for robust frameworks to prevent financial crime, such as making “wallet hopping” – moving funds rapidly through a long series of intermediary digital wallets to obscure their original source – by money launderers more difficult and more detectable.

Attendees argued for a principles-based regulatory approach, given that the market is still developing and it is difficult to predict viable business models.

Some suggested offering temporary regulatory relief, such as reduced requirements for low-volume stablecoin activity, provisional licences or a “corporate opt-out” for sophisticated customers.

The need for interoperability was a point of debate, with some seeing it as a key goal, but others arguing that seamless technical interoperability is not immediately necessary for stablecoins to be useful.

One way to enable interoperability might be to remove barriers for financial institutions, such as punitive capital requirements and duplicative anti-money laundering and counter-terrorism financing (AML/CTF) registrations.

An overall point that came out of the sprint was that stablecoins represent a significant opportunity to ensure that the UK remains a key financial hub. A well-regulated regime would attract global businesses and could make the British pound more competitive in the digital economy.

Strengthening the regulatory approach

The development of the UK's stablecoin framework will continue over the coming months as the FCA seeks to finalise its rules for issuers by mid-2026.

The insights from the sprint will feed into the wider efforts to overhaul UK payments regulation under the National Payments Vision (NPV).

Agant’s Rhodes noted that, “It's still far too early to predict all the operational practicalities, because use cases and business models are still developing. But these industry sessions help identify the challenges with getting new technology and new products off the ground.”

The regulator is scheduled to host a follow-up roundtable in May, this time focusing specifically on trade payments, including business-to-business (B2B) use cases, trade finance applications and related domestic and international payment flows.

The process will be interesting to watch, particularly given sprint attendees’ recommendation that the FCA should formally treat stablecoins as payment instruments rather than cryptoassets.

In theory, the regulator will use the end-to-end user journeys and risk mitigations stress-tested during the sprint to strengthen its approach, helping to ensure that its policies support market innovation while underpinning consumer confidence and safety.

For now, payments firms should be considering practical questions about how traditional payment mechanics will work on decentralised infrastructure.

This includes determining how consumers will actually access stablecoins to make purchases – via existing payment cards, pass-through digital wallets or self-custody tokenised wallets – and how privacy and data protection obligations will apply to on-chain activities.

Financial institutions’ adoption of stablecoins is still largely cautious and experimental due to barriers such as punitive capital requirements and duplicative AML/CTF registrations. However, firms should be ready to act if regulators introduce the sort of temporary relief measures discussed at the sprint.

They should also consider participating in or monitoring the FCA’s Regulatory Sandbox stablecoins cohort to test UK-issued stablecoins.

As they develop their strategies, firms should prioritise consumer protection and ensuring that consumers using stablecoins have access to the same levels of protection and safeguards that they would expect from traditional fiat payments.

Above all, the sprint showed that baking trust into the system is seen as essential for any stablecoin innovation to scale safely.