.svg)

The ninth edition of the UK’s Regulatory Initiatives Grid, published in December 2025, sets out the country’s financial services regulatory agenda for the next two years.

The grid is intended to help the UK financial sector and stakeholders plan for regulatory changes that could have an operational impact. For example, it highlights regulators’ priorities, which include regulatory streamlining and consumer protection.

Financial institutions operating in the UK can find insights in the grid into what the regulators will be prioritising over the coming months, what consultations they should consider responding to and how the regulatory environment could change.

In this piece, Vixio examines what the regulators have outlined in the multi-sector section of the latest regulatory grid, explains the likely impact of developments on financial institutions and suggests what the regulators’ stated priorities tell us about the direction of travel in the UK.

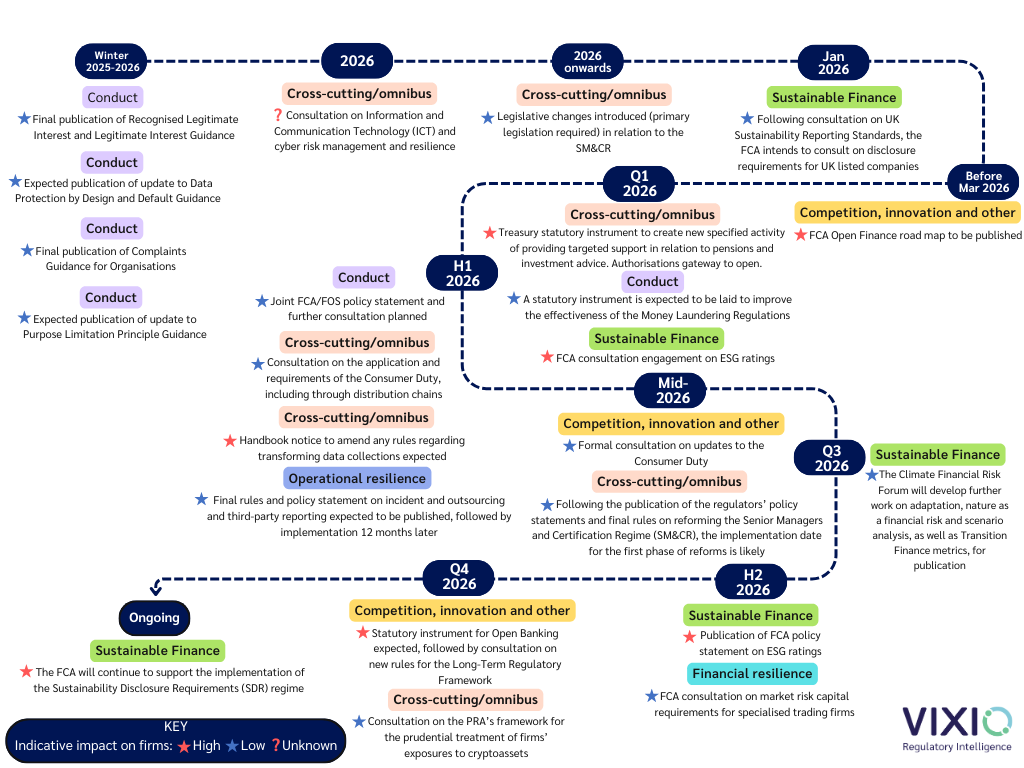

Timeline for 2026 (download here)

|

Regulator and Initiative |

Why should you care? |

Rating, Deadlines and Resources |

|

Competition, innovation and other |

||

|

FCA Review of FCA requirements following the introduction of the Consumer Duty In 2024, the FCA published a call for input on simplifying Consumer Duty requirements to support innovation, reduce costs and maintain consumer protection. In September 2025, the FCA published an update that set out next steps, including publishing a consultation paper on targeted clarifications of FCA rules and guidance and reviewing historic non-Handbook publications. |

The FCA is aiming to reduce complexity and the compliance burden for firms without diluting consumer protection standards. Initiatives such as streamlining rules, modernising disclosures and clarifying advice/guidance boundaries could materially affect UK-regulated firms’ product design, customer journeys and communications. Although these reforms increase clarity, firms will remain subject to rigorous scrutiny under the Consumer Duty. Early engagement with the consultation and proactive assessment of internal processes will be critical for ensuring compliance and minimising supervisory risk. |

The FCA expects to communicate policy outcomes and next steps in H1 2026. Relevant Resources |

|

FCA/HMT Smart Data: Open Banking and Open Finance The Data (Use and Access) Act grants HMT the powers necessary to make secondary legislation establishing Smart Data schemes for financial services. This will enable the FCA to implement a long-term regulatory framework for open banking and potentially extend it to broader open finance initiatives across other sectors. |

Smart Data is how the UK plans to evolve from open banking to open finance. This means extending data sharing beyond finance into sectors such as energy, broadband and retail. Firms required to share data will face new governance, consent-management and liability challenges, and firms able to ingest and monetise cross-sector data may gain pricing and distribution advantages. Early architectural decisions on data infrastructure and partnerships will shape long-term competitiveness. Firms should monitor developments, as Smart Data will bring new compliance requirements and risks for businesses required to share data and create commercial opportunities for businesses looking to exploit such data. Key steps include assessing potential impacts on data governance and customer propositions and considering strategic responses to emerging Smart Data frameworks. |

The FCA’s open finance road map is due to be published by March 2026. The statutory instrument for open banking is expected to be laid in Q4 2026, with the FCA consulting on new rules for the Long-Term Regulatory Framework shortly after. Relevant Resources

|

|

FCA/PSR Open Banking - Joint Regulatory Oversight Committee actions The Joint Regulatory Oversight Committee (JROC), chaired by the FCA and PSR, and also comprising the Treasury and the CMA, previously had responsibility for developing open banking in the UK. The National Payments Vision (NPV) makes the FCA the lead regulator for open banking, consolidating oversight and future development of the framework. |

A key next phase of open banking in the UK is the introduction of variable recurring payments (VRPs), a payment mechanism that allows users to securely authorise trusted third parties to manage recurring transactions with flexible amounts and intervals. As the FCA assumes full oversight, firms can expect targeted engagement on its regulatory framework and evolving legislative powers. Although VRPs could reduce reliance on cards and improve customer experience, they also introduce settlement, fraud and liability questions that firms will need to resolve within a clearer, but potentially stricter, regulatory perimeter. Effective adoption of VRPs and alignment with the FCA’s guidance may present operational and compliance challenges, but will also create opportunities for innovation in payments and consumer experience. |

The FCA will provide a progress update in Q4 2025. VRP goes live in H2 2025. Relevant Resources |

|

Conduct |

||

|

ICO Recognised Legitimate Interest and Legitimate Interest Guidance The ICO will provide new guidance and update existing guidance due to changes introduced by the Data Use (and Access) Act, following on from a consultation launched on August 21, 2025. |

The Data Use (and Access) Act introduced changes to the lawful bases of recognised legitimate interest and legitimate interest. The new guidance aims to assist UK organisations on the use of recognised legitimate interest for UK GDPR purposes. The updated guidance will narrow firms’ discretion in relying on recognised legitimate interest. Firms that currently depend on this basis for analytics, fraud prevention or product development may face heightened enforcement risk if their assessments are not robustly documented and aligned with the ICO’s revised interpretation. |

Winter 2025/2026: Final publication expected. Relevant Resources |

|

FCA Modernising the redress framework and external redress guidance The FCA published a joint Consultation Paper with the Financial Ombudsman Service (FOS) with several proposals to modernise the redress system so it better serves consumers and provides greater certainty for firms to invest and innovate. The Treasury published a Consultation Document on potential legislative changes to enhance regulatory coherence and alignment between FOS and FCA for the benefit of consumers and firms. The consultations closed in October 2025 and the FCA is currently working with the Treasury and the FOS to review responses and determine next steps. |

The FCA’s proposals aim to modernise the redress framework to better serve consumers and give firms greater certainty to invest and innovate. In particular, the proposals would:

Firms should monitor developments and consider whether existing complaints handling policies and record-keeping arrangements would remain appropriate under the proposed changes. If implemented, the reforms could materially reshape firms’ complaints risk profile, particularly through the introduction of a longstop and changes to Financial Ombudsman Service (FOS) decision-making. Firms should expect close scrutiny of how complaints frameworks adapt, especially in the context of mass redress events. In any case, firms should expect a modernised and clearer redress framework. |

The FCA expects a key milestone to arrive in Q1 2026. A joint FCA/FOS policy statement and a further consultation is expected to be published in H1 2026. Relevant Resources |

|

HMT Consultation on Improving the Effectiveness of the Money Laundering Regulations On March 11, 2024, HMT launched a consultation on improving the effectiveness of the Money Laundering Regulations (MLRs). Following this, it announced a package of forthcoming legislative changes, as well as guidance. |

The consultation was part of HMT’s commitment to reduce money laundering, which was set out in the Economic Crime Plan 2023-26. The forthcoming legislative changes aim to:

The changes are technical in nature, aiming to improve the effectiveness of the regulation and to ensure proportionality for both regulated firms and customers. They may require firms to re-engineer elements of customer due diligence and governance Given the upcoming statutory instrument, firms should begin reviewing existing AML frameworks and governance arrangements to identify areas likely to be affected by the proposed changes, particularly in relation to customer due diligence. |

A statutory instrument is expected to be laid before Parliament in Q1 2026. Relevant Resources |

|

ICO The ICO is committed to updating the automated decision making and profiling guidance. |

The updated guidance aims to explain how UK data protection law applies when organisations use automated decision-making and profiling, taking into account the amendments introduced in the Data (Use and Access) Act. In particular, the guidance covers scenarios where firms use a client’s personal data to automatically approve or deny them for financial products and services. This guidance will help firms to understand if they are engaging in automated decision-making, and if so, their responsibilities under the UK GDPR. Upon final publication, firms should consider the updated guidance when assessing whether their use of automated decision-making and profiling aligns with UK GDPR requirements. |

A public consultation is expected to be launched in Winter 2025/2026 with final publication expected in Spring 2026. Relevant Resources |

|

ICO Data Protection by Design and Default Guidance Update The ICO is committed to updating its guidance on data protection by design and default. |

The ICO is revising its existing guidance on data protection by design and default to incorporate changes introduced by the Data (Use and Access) Act. The updated guidance will include the new duty for providers of online services likely to be accessed by children. When implementing data protection by design, providers of these services will need to consider how they can best support and protect children and take into account their needs at different ages and stages of development. Firms will need clear escalation, documentation and governance arrangements. They face increasing operational burden but also greater regulatory exposure if processes are poorly implemented. |

A key milestone is expected in Q1 2026, with final publication in Spring 2026. Relevant Resources |

|

ICO Complaints Guidance for Organisations The Data (Use and Access) Act introduces a new requirement for organisations to have a process in place to deal with data protection complaints. To help support organisations, the ICO’s new draft guidance sets out the new requirements and what they must, should and could do to comply. |

The upcoming finalised guidance aims to walk organisations through the new requirements contained in the Data (Use and Access) Act. It also aims to inform organisations of what they must, should and could do to comply. In particular, the draft guidance addresses:

The guidance further includes tips and practical advice for each stage of the process, improving clarity for relevant firms, which should review the information and update their policies and procedures accordingly. |

A key milestone is expected in Q1 2026, with publication of the finalised guidance in Winter 2025/2026. Relevant Resources |

|

ICO International Transfers Guidance The ICO will be publishing new and updated guidance on international transfers, making it quicker and easier for businesses to transfer data safely. The guidance will also reflect the new requirements contained in the Data (Use and Access) Act. |

The new and updated guidance aims to make it quicker and easier for businesses to transfer data safely. The guidance also reflects the changes introduced in the Data (Use and Access) Act. The updated guidance will set out the key requirements. It aims to reduce complexity and support the responsible transfer of personal information. Firms should consider how the updated guidance may affect their data transfer practices, ensuring processes and controls remain robust and proportionate. Changes may reduce friction for some transfers, but misalignment with the updated framework could expose firms to enforcement risk. |

A key milestone is expected in Q1 2026, with publication of the finalised guidance in Winter 2025/2026. Relevant Resources |

|

ICO Purpose Limitation Principle Guidance Update The ICO will be publishing updated guidance in order to account for the changes introduced in the Data (Use and Access) Act. |

The updated guidance will provide amendments to the existing provisions that set out when an organisation can consider a new use case for personal information to be compatible with the original purpose it collected it for. This will constrain how firms repurpose personal data for new use cases, particularly in analytics and product development. Upon final publication, firms should compare their own practices against the updated guidance. |

Publication of the finalised guidance is expected in Winter 2025/2026. Relevant Resources |

|

Cross-cutting/omnibus |

||

|

HMT Gibraltar Authorisation Regime (GAR) Following the UK and Gibraltar leaving the EU, the UK is establishing a new market access framework for Gibraltarian firms. The GAR was introduced in the Financial Services Act 2021, but a framework of secondary legislation is needed to operationalise the regime. This is currently under development. |

New entrants looking to passport inwards to the UK from Gibraltar, or vice versa, should monitor developments to understand how they will be able to do so under the GAR. Existing financial entities utilising the temporary permissions programme should be aware that the current regime is due to end in December 2026, after which their permissions will lapse (subject to any further extensions). |

Authorities have extended temporary passporting arrangements until December 31, 2026. Relevant Resources |

|

FCA Complaints Reporting Review In December 2025, the FCA published Policy Statement 25/19, which implemented changes such as six-monthly reporting, removal of group reporting and simplified nil returns. Furthermore, the FCA has an ongoing consultation on extending customer vulnerability data points reporting to payment services, funeral plans and claims management companies (CMCs), within the new consolidated return. |

Firms need to ensure that they are operationally ready to implement the changes outlined in PS 25/19 before the first relevant reporting period begins, to ensure compliance. Should the FCA confirm the extension of vulnerability data point capture, PSPs will also need to ensure internal identification and treatment of vulnerability aligns to the FCA’s guidance and four drivers: health, life events, resilience and capability. |

Simplified complaints reporting process takes effect from January 1, 2027. Relevant Resources |

|

FCA Non-financial misconduct (NFM) in financial services firms On December 12, 2025, the FCA published its policy statement confirming its final guidance on non-financial misconduct (NFM) and related amendments to its Code of Conduct (COCON) Sourcebook. The changes include:

|

The additional guidance on the definition of NFM is likely to make it easier for firms to interpret and consistently apply the FCA’s rules on non-financial misconduct. Firms should review their existing policies and practices against the revised handbook to ensure they remain compliant and are taking appropriate action against breaches. In particular, non-bank firms that are authorised under FSMA 4a permissions should take particular care to ensure that their policies are compliant with the expanded scope of COCON rules for their firm type. |

The guidance and new rule comes into effect on September 1, 2026. Relevant Resources |

|

FCA Consumer Duty scope and distribution chain The FCA continues to prioritise the Consumer Duty, using it as a flexible tool rather than introducing new prescriptive rules. The regulator is consulting on amending rules on client categorisation and conflicts of interest, following a December 2025 supervisory statement on firms’ responsibilities under the Duty for distribution changes. |

The FCA’s approach reinforces the Consumer Duty as a flexible supervisory tool. The planned changes clarify how the Duty should be applied in practice, particularly around client categorisation, conflicts of interest and distribution arrangements. The Consumer Duty is one of the most broad-ranging pieces of regulation in the UK industry, and firms stand to benefit from greater clarity. |

The consultation on amending rules regarding client categorisation and conflict of interest closes on February 2, 2026. A consultation on the Duty’s application and requirement across distribution chains is expected in H1 2026. Relevant Resources |

|

PRA Framework for the prudential treatment of firms’ exposures to crypto-assets The PRA is developing changes to its rules to implement the Basel standard for the prudential treatment of firms’ exposures to crypto-assets. |

The upcoming consultation provides a chance for firms to provide feedback straight to the authorities, ensuring that the draft rules will align with global Basel standards and the FCA’s broader UK regime for crypto-asset firms. This will be crucial for international firms which are hoping to reduce operational burden where possible. |

A consultation paper expected in Q4 2026. Relevant Resources |

|

FCA/HMT Appointed Representative regime legislative reforms In August 2025, the Treasury published a policy statement on the Appointed Representatives (AR) regime, outlining plans to adapt its legislative framework to introduce the following changes:

HMT, working with the FCA, will develop a detailed proposal for design and implementation of the principal permission and will consult on the proposal in due course. |

The UK's AR regime allows firms to conduct certain financial activities without direct authorisation by acting under the responsibility of a fully authorised “principal” firm. Firms currently operating as an AR should be aware that they will soon be liable to greater consumer protections obligations. Consumers will be able to lodge complaints against them with FOS. Authorised firms should await the upcoming consultation and be aware that they may need to obtain permission from the FCA to use the AR regime. |

Expected upcoming consultation, no date proposed yet. Relevant Resources |

|

FCA/HMT Advice Guidance Boundary Review The Advice Guidance Boundary Review sets out the FCA’s and Treasury’s proposals to close the gap in pensions and investments advice. Targeted support introduces a new set of conduct standards, which, alongside the Consumer Duty, provide consumer protections. |

Firms will need to apply for permission to conduct the proposed new targeted support “new specified activity”. The FCA is on track to enable firms to begin applying for permission to provide targeted support from March 2026, before the new rules are expected to come into effect on April 6, 2026, subject to legislation to create a new specified activity for targeted support. Firms entering this space face first-mover opportunity, but also regulatory risk if operational boundaries between advice and guidance are poorly controlled. |

HMT’s statutory instrument will be laid and the authorisations gateway open between January and March 2026. The rules are expected to come into effect on April 6, 2026. The FCA is planning to further consult on simplifying and consolidating our investment advice rules and guidance in early 2026. Relevant Resources |

|

FCA/PRA Berne Financial Services Agreement (BFSA) The Berne Financial Services Agreement (BFSA) is a mutual recognition agreement between the UK and Switzerland. It facilitates cross-border financial services trade, providing new market access in selected areas and securing existing levels of access in certain others. |

UK investment and insurance firms looking to expand their services into Switzerland and vice versa should consider taking advantage of the agreement and apply via the notification forms of the various authorities. This approach recognises supervisory and regulatory regimes of the UK and Switzerland as being of a similarly high standard, removing the need for businesses to navigate unfamiliar rules through greater alignment. The BFSA creates new cross-border opportunities, but firms must ensure ongoing compliance with notification, reporting and supervisory expectations |

The BFSA took effect on January 1, 2026. BFSA firms’ annual reporting commences from Q2 2027. Relevant Resources |

|

PRA/BoE Information and Communication Technology (ICT) and cyber risk management and resilience To further enhance the sector’s operational resilience capabilities, the Bank and the PRA intend to consult on policy relating to the management of ICT and cyber risks. |

Firms should look out for the upcoming consultation paper, which is likely to propose new regulatory obligations on firms to strengthen cyber risk management and resilience. |

A consultation paper is expected to be issued during 2026. Relevant Resources |

|

FCA/PRA/BoE Transforming Data Collections Regulators have been working to improve the data collections process for firms through:

|

Organisations should benefit from the streamlined regulatory reporting across the different financial services authorities, given the deletion of a number of regulatory reports, although they face transition risk as legacy processes are retired. Firms must ensure that their compliance teams have been updated alongside their operational process, and are using the latest regulatory reporting templates as provided by the regulators. |

Relevant amendments to the FCA handbook rules are expected in H1 2026. Relevant Resources |

|

FCA/PRA/HMT Reforms to the Senior Managers and Certification Regime (SM&CR) The ambition is to reduce the regime’s burden by 50 percent, while preserving accountability. The legislative changes that HMT plans to introduce will enable the regulators to further streamline the regime as part of an anticipated second phase of reforms. |

Firms will likely benefit from the streamlined regime and should keep a lookout for an update from HMT on the introduction of the proposed legislative changes alongside the final policy statement, rules and implementation dates in 2026. They should expect increased supervisory focus on outcomes rather than process. Transitional uncertainty may create short-term compliance risk until final rules and timelines are confirmed. |

Legislative changes will be introduced from 2026 onwards. The implementation date has yet to be confirmed, but is slated for mid-2026. Relevant Resources |

|

Sustainable finance |

||

|

HM Treasury/FCA ESG ratings regulation In November 2024, HM Treasury published its consultation response and draft legislation to bring ESG rating providers into regulation. Following analysis of technical comments on the draft legislation, HM Treasury laid the draft legislation before parliament on October 27, 2025. Once it is formally made (after debates and parliamentary approval), the legislation will expand the FCA’s regulatory perimeter to include ESG ratings. The FCA has published its consultation on the regulatory regime for ESG ratings providers, focusing on transparency, good governance, robust conflicts management and effective systems and controls. |

The new regulatory regime aims to address issues raised around transparency, including unclear and confusing information; weaknesses in rating providers’ systems and controls, such as outdated or incomplete data and estimates; inadequate governance arrangements; and existing and potential conflicts of interest. By ensuring there are more oversight and controls on this sector, the FCA can address these concerns, leading to more confidence in decisions and more trust and credibility in relation to the UK market’s reputation regarding sustainable finance. This, in turn, should make the market more attractive for investment. As the proposed regime is also grounded in IOSCO recommendations published in 2021, it will also ensure that the UK remains aligned with global standards. |

The FCA’s consultation paper (CP25/34: ESG ratings: proposed approach to regulation) closes on March 31, 2026, with the policy statement expected to follow in H2 2026. A 12-month application window is expected to open in June 2027, with the regime coming into effect from June 2028. Relevant Resources |

|

FCA Sustainability Disclosure Requirements (SDR) and investment labels The FCA has introduced a sustainable classification and labelling system for investment products. This will help consumers navigate the sustainable investment landscape and find products meeting their sustainability preferences. Firms have been able to use investment labels since July 2024, with the accompanying disclosures also becoming applicable. |

Firms are required to provide standalone consumer-facing disclosures summarising a product’s key sustainability requirements. The disclosure must be presented in a prominent place on the product’s webpage, app or other digital medium. This disclosure must be reviewed at least every 12 months. Although the FCA decided in April 2025 not to proceed with extending the regime to portfolio managers at that time, there was broad support for this change to improve consumer outcomes, and therefore such firms should be prepared for this being put back on the agenda. However, although the FCA has flagged these changes as high impact, it has not committed to providing further specifics on what it plans to do in relation to SDRs in 2026, and at the moment just says its work is ongoing. |

Relevant resources

|

|

FCA/PRA Climate Financial Risk Forum In 2019, the FCA and PRA jointly established the Climate Financial Risk Forum (CFRF), which brings together senior financial sector representatives to share their experiences in managing climate-related risks and opportunities. The CFRF continues to work to produce guidance and best practice materials for the financial sector. |

In 2026, the CFRF is expected to build on the guidance and tools it has established on the key themes of adaptation, nature as a financial risk and scenario analysis. The CFRF is also looking to develop Transition Finance metrics for publication in Q3 2026. As physical climate risks are ever increasing, the forum is now looking to help the financial industry move beyond just creating high-level strategies into establishing practical, operational responses, and integrating resilience into decision-making. Although the CFRF is an advisory forum, it does provide recommendations to policy makers. Monitoring developments can ensure financial institutions are informed of the potential direction of travel in relation to environmental risk policy as early as possible. It can also help ensure alignment across the industry. |

Relevant resources Information on the CFRF can be found here on the FCA’s website and here on the Bank of England’s website. |

|

Financial resilience |

||

|

FCA Market risk capital requirements for specialised trading firms The FCA is reviewing market risk capital requirements for MiFIDPRU investment firms that deal on their own account. In a December 2025 engagement paper, the regulator outlined seven potential approaches to updating the framework, including margin-based and internally modelled approaches, reflecting the view that such investment firms pose lower systemic risk than banks. |

Market risk capital requirements ensure firms can absorb losses when market positions move against expectations, supporting both firm resilience and overall market integrity. The FCA’s review aims to make the framework more proportionate, reduce barriers to entry and promote liquidity in wholesale markets. For specialised trading firms, this could lower capital costs, enable more efficient risk management and encourage participation in trading activity. Firms should monitor the consultation closely and assess potential impacts on capital planning, trading strategies and internal risk models. |

The deadline for responses to the engagement paper is February 10, 2026. A consultation paper is due in H2 2026 and a policy statement in 2027. Relevant Resources |

|

Operational resilience |

||

|

FCA/PRA Incident and Outsourcing and Third-Party Reporting The purpose of this proposed policy is to introduce clarity regarding the information firms should submit when operational incidents occur, as well as collect certain information on firms’ outsourcing and third-party arrangements. This will help to manage the risks they may present to the PRA/FCA’s objectives, including resilience, concentration and competition risks. |

The aim of introducing new regulations in relation to reporting operational incidents and material third-party arrangements is to minimise the disruption caused to operations, and therefore consumers, by events such as IT outages or cyber-attacks. All regulated firms and payment service providers will be required to report on operational incidents. Authorised payment institutions and electronic money institutions, as well as banks, are included within the scope of those who will be required to report on third-party arrangements. The proposals significantly increase reporting and judgment risk, requiring firms to define materiality thresholds without prescriptive metrics. Although this will be burdensome, failure to comply could carry greater supervisory and reputational costs than the reporting itself. |

FCA policy statement and final rules are expected to be published in H1 2026 (and then come into effect 12 months later). Relevant Resources The FCA and PRA launched consultations on December 13, 2024, which then closed on March 13, 2025: |

|

Repeal and replacement of assimilated law under FSMA 2023 |

||

|

FCA/HMT Review of the Benchmarks Regulation As part of the Financial Services Growth and Competitiveness Strategy, the government committed to reforming the UK Benchmarks Regulation (BMR) to reduce burdens on UK firms. |

The government is considering repealing the Benchmarks Regulation and replacing it with a lighter touch regime focusing on the benchmarks and administrators that may pose systemic risks to UK financial markets. Under the proposals, benchmarks and benchmark administrators will be designated by HMT with advice from the FCA. Only these designated firms will be subject to the new regime – other benchmarks and benchmark administrators will not be regulated. This could reduce the number of regulated benchmark administrator firms by more than 80%. |

Responses to a consultation paper are due by March 11, 2026 Relevant Resources |