The Vixio Voice

Actionable insights for the world’s most complex regulated markets

Want to quickly brush up on industry trends, insights, or emerging regulatory changes?

We've summarised a range of topics to help you get a better grasp of what's important to know.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

Ready to explore the future of RegTech with us, in a city near you?

Meet our team of experts at RegTech, Financial Services and Gambling events around the globe

Want to be the first learn about the latest regulatory updates and developments?

Our thought-leadership webinars feature industry experts, interactive demos for compliance leaders across the Financial Services and Gambling industries

.png)

%2520(3).png)

.png)

.png)

.png)

.png)

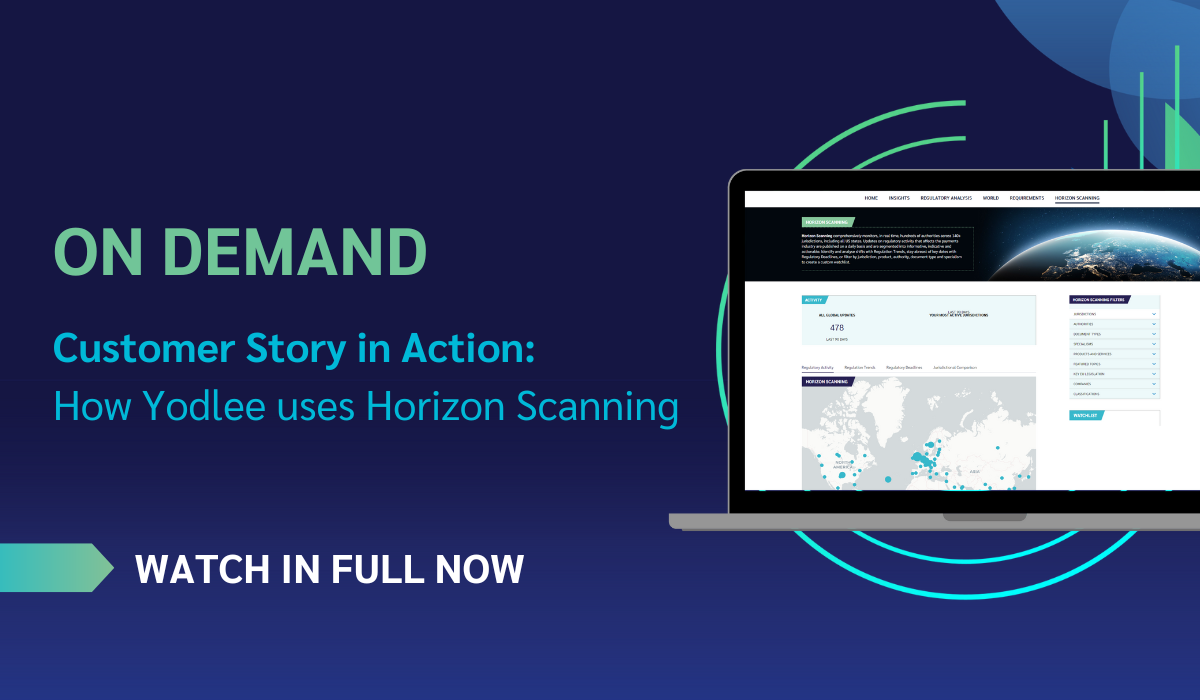

Want to see how industry leaders like you solve their RegTech challenges?

Learn more from our global clients about how they use Vixio to stay ahead in an ever-evolving regulatory landscape

Want to stay ahead of your competition with the most up to date regulatory information?

Read the latest independent outlook reports and guides on industry trends and thought-leadership for the gambling and financial services sectors

.png)

.png)

.png)

.png)

.png)

Want to quickly brush up on industry trends, insights, or emerging regulatory changes?

We've summarised a range of topics to help you get a better grasp of what's important to know.

.png)

.png)

.png)

.png)

Ready to explore the future of RegTech with us, in a city near you?

Meet our team of experts at RegTech, Financial Services and Gambling events around the globe

Want to be the first learn about the latest regulatory updates and developments?

Our thought-leadership webinars feature industry experts, interactive demos for compliance leaders across the Financial Services and Gambling industries

.png)

Want to see how industry leaders like you solve their RegTech challenges?

Learn more from our global clients about how they use Vixio to stay ahead in an ever-evolving regulatory landscape

Want to stay ahead of your competition with the most up to date regulatory information?

Read the latest independent outlook reports and guides on industry trends and thought-leadership for the gambling and financial services sectors

.png)

Want to quickly brush up on industry trends, insights, or emerging regulatory changes?

We've summarised a range of topics to help you get a better grasp of what's important to know.

.jpeg)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.gif)

.png)

Ready to explore the future of RegTech with us, in a city near you?

Meet our team of experts at RegTech, Financial Services and Gambling events around the globe

Want to be the first learn about the latest regulatory updates and developments?

Our thought-leadership webinars feature industry experts, interactive demos for compliance leaders across the Financial Services and Gambling industries

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

Want to see how industry leaders like you solve their RegTech challenges?

Learn more from our global clients about how they use Vixio to stay ahead in an ever-evolving regulatory landscape

Want to stay ahead of your competition with the most up to date regulatory information?

Read the latest independent outlook reports and guides on industry trends and thought-leadership for the gambling and financial services sectors

.png)

.png)

%2520(1).png)

.png)